Nigeria has emerged as Africa’s no.1 crypto economy, defying economic challenges and regulatory hurdles. What drove Nigeria to No.1 in Africa? Did the Nigerian economy get better in the last one year?

If available data is anything to go by, Nigeria’s worsening economic situation and presently comatose crypto regulatory stance might have pushed more and more Nigerians into embracing decentralized cryptocurrencies as an alternative at a time when distrust in its economic managers increased significantly.

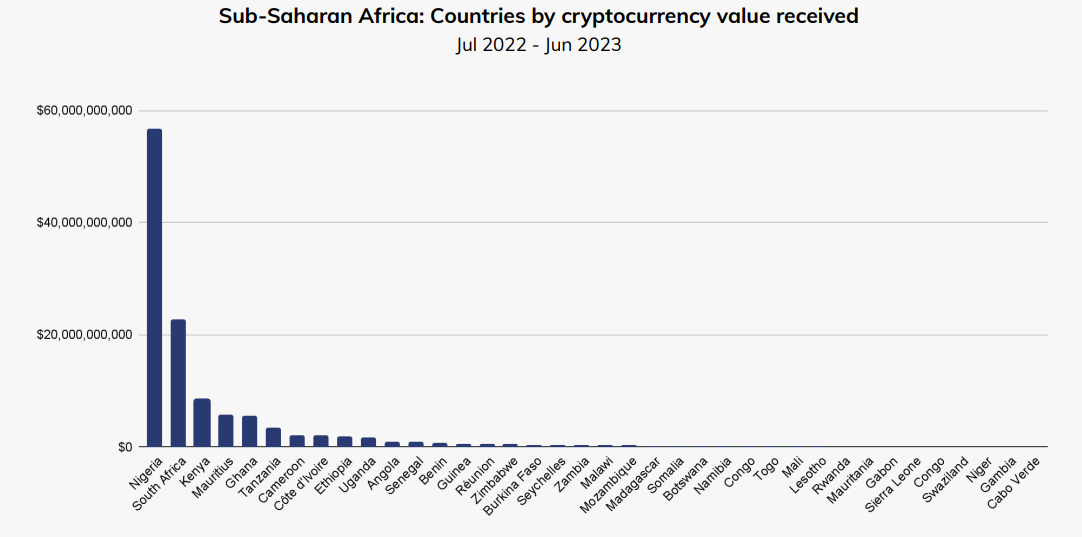

According to the just-released The Chainalysis 2023 Geography of Cryptocurrency Report, Nigeria has attained the No.1 position in the crypto economy on the continent. Of the estimated $117.1 billion in on-chain value received by Sub-Saharan Africa within July 2022–June 2023 (representing only 2.3% of the global transaction volume), Nigeria received nearly $60 billion dollars. This value is considerably more than what South Africa, Kenya, Mauritius, and Ghana received.

Nigeria takes the lead in the African crypto economy, regardless of regulatory restrictions in the country.

Over the years, Nigeria has carved its niche as a powerhouse in the African crypto arena. Against all odds, particularly regulatory restrictions since February 2021 when the Central Bank of Nigeria (CBN) shut the window to the country’s banking and financial sector against crypto-related transactions, Nigeria’s crypto economy has shown remarkable resilience.

Third to only Saudi Arabia and Vietnam, Nigeria is one of only six countries globally where year-on-year growth in crypto transaction volume is placed at a growth rate of 9.0%. This impressive growth, amidst market turmoil, including plummeting oil prices and deepening socio-economic challenges.

Economic challenges fuel Nigeria’s crypto adoption.

The Chainalysis report acknowledges that Nigeria’s journey into the cryptocurrency space is traceable to the country’s economic hardships.

Since 2016, Nigeria has grappled with two major recessions, further exacerbated by political instability, COVID-19 pandemic, and oil price collapse. The uncertainty created by these crises has resulted in high unemployment rates and the increasing number of Nigerians seeking better opportunities abroad.

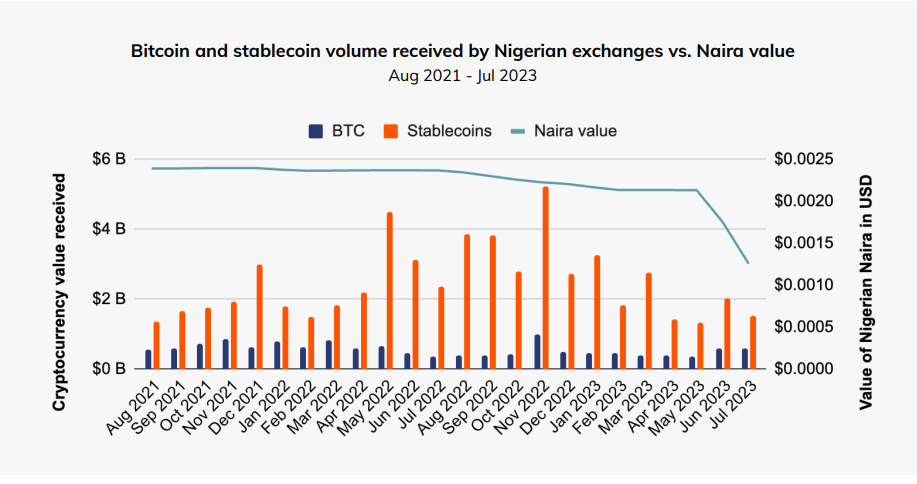

In particular, the Naira crisis, compounded by the CBN’s decision to redesign the local currency, triggered an acute cash shortage, making the use of old notes uncertain. This occurred alongside a nationwide election period and a record high inflation rate, exceeding 20.0% in early 2023. As a result, in light of the unpredictable economic conditions prevailing in Nigeria, a number of Nigerians sought solace in cryptocurrencies, particularly stablecoins, as a hedge against rising inflation and the depreciation (and devaluation) of the local currency. Others who trusted otherwise volatile cryptocurrencies such as bitcoin, Ethereum, etc—purely driven by market forces—invested in these assets.

The clear connection between the depreciation of the Naira and the growing fascination with cryptocurrencies may be unmistakable. As the Naira value dwindled, interest in bitcoin and stablecoins soared, especially during significant drops in June and July of 2023, the report shows. These periods of high activity were influenced by users seeking to capitalize on the volatility resulting from specific events rather than purely reacting to local economic issues.

Inflation feeds crypto adoption in Nigeria, and so does its youthful demography.

A report by Business Day underscores the turbulence in the Naira’s performance in the financial market. The Naira has depreciated by 40% since June, largely eroding investor trust. The CBN’s approach of maintaining negative real interest rates may have also intensified the demand for the US dollar.

Cryptoiz Research also highlights that high inflation is a primary driver behind the growing adoption of cryptocurrencies in Nigeria. Given the surge in inflation, an increasing proportion of Nigerian citizens, specifically the younger population segment, have turned to alternative forms of assets like bitcoin and stablecoins as a means to safeguard their financial reserves from the depreciation of domestic currency.

Beyond inflation, the youthful and increasingly techy population of Nigeria, averaging 18 years, continues to also spur crypto adoption in the country. Curiosity for bitcoin or cryptocurrencies generally, as well as the way these decentralized currencies have created immense opportunities for others, has partly sustained interest in them.

A report CoinGecko revealed Nigeria as the country most interested in cryptocurrency since the market crash in April 2022. This interest is measured by the population’s high search levels for cryptocurrency-related terms. With a total search score of 371, Nigeria tops the list for its citizens’ interest in phrases like ‘cryptocurrency,’ ‘invest in crypto’, and ‘buy crypto’ on a worldwide scale. Additionally, Nigerians have shown a strong curiosity in specific cryptocurrencies, with ‘Solana’ being a prominent keyword in their searches.

You might also like: February 5: Nigeria’s blockchain association launches ‘Crypto is Legit’ on the Anniversary of CBN Ban; says “regulate crypto, not ban”

Resilience in the Face of Regulatory Challenges

Nigeria’s crypto market has managed to thrive despite regulatory hurdles. As mentioned earlier, the CBN restricted banks and other financial institutions in the country from facilitating in cryptocurrency-related transactions. But this move, as available data shows, has not curbed crypto transactions in the country. On the contrary, Nigeria’s cryptocurrency market has consistently grown, particularly in peer-to-peer (P2P) and over-the-counter (OTC) crypto transactions. Nigeria leads as a significant player in the crypto economy in Sub-Sahara Africa.

You might also like: Nigeria approves national blockchain policy, but crypto remains in limbo

Recent developments in Nigeria, however, indicate a likely positive shift in the regulatory landscape. In June, the Nigerian government approved its National Blockchain Policy, followed by a policy dialogue in September, involving the blockchain industry led by the Stakeholders in the Blockchain Technology Association of Nigeria (SIBAN) and the National Information Technology Development Agency (NITDA). The deliberations underscored the significance of implementing progressive policies that would expedite the incorporation of blockchain technology across various sectors of the Nigerian economy.

If data is anything to go by, it is time the National Blockchain Policy Steering Committee, which includes the CBN, took definite and conclusive steps concerning the CBN stance on cryptocurrency in Nigeria. This calls for risk-based regulation, not ban. It is yet another call for both regulators and operators to work together, not apart. Technology is neutral. For fair, inclusive, and transparent markets, regulation should not be different. It is time Nigeria crypto regulation got out of coma.

Credit: Solomon Victor is a Technical Analyst who is also knowledgeable about various aspects of blockchain and cryptocurrency.

Discover more from Crypto Asset Buyer

Subscribe to get the latest posts sent to your email.