By Jude Ayua

The International Monetary Fund (IMF) published a paper in September 2024 to advise countries on central bank digital currencies (CBDC) adoption. Prepared by Tayo Tunyathon Koonprasert, Shiho Kanada, Natsuki Tsuda, and Edona Reshidi, the paper discloses strategies that policymakers can use to achieve early CBDC adoption. It advises that successful CBDC adoption requires technical readiness, operational robustness, strategic policy, and design choices that target end-user and intermediary involvement from its inception. In addition, beyond simply creating a CBDC, central banks should proactively engage stakeholders to facilitate adoption.

Challenges facing CBDC adoption

The IMF paper found that CBDC adoption remains “slow and limited” among the countries that have launched a CBDC or are conducting large-scale pilots due to various challenges. The major challenges identified are as follows:

- lack of public awareness and trust;

- preference for existing payment methods; and

- inadequate incentives for intermediaries.

The three jurisdictions that have launched a CBDC are the Bahamas, Jamaica, and Nigeria. In the Bahamas, the challenges limiting its CBDC (Sand Dollar) adoption include a lack of merchant participation, lack of integration with the traditional banking system, and inadequate education of users about the benefits and usage of the Sand Dollar. In Nigeria, the IMF noted that its CBDC, eNaira’s slow adoption is partially because of the Central Bank of Nigeria (CBN)’s phased approach, as it initially granted access only to customers with bank accounts and restricted eNaira transactions to domestic use.

The jurisdictions that have initiated large-scale CBDC pilots include China, the Eastern Caribbean Currency Union (ECCU), and India. The ECCU’s CBDC (DCash) has faced the challenges of “shortcomings in user education,” the Eastern Caribbean Central Bank’s lack of oversight in developing an adequate merchant network from the onset, and the non-integration of DCash with merchant point-of-sale (POS) devices and ECCU’s legacy financial systems contributed to its lower adoption.

Read also: Introduction to Central Bank Digital Currencies (CBDCs)

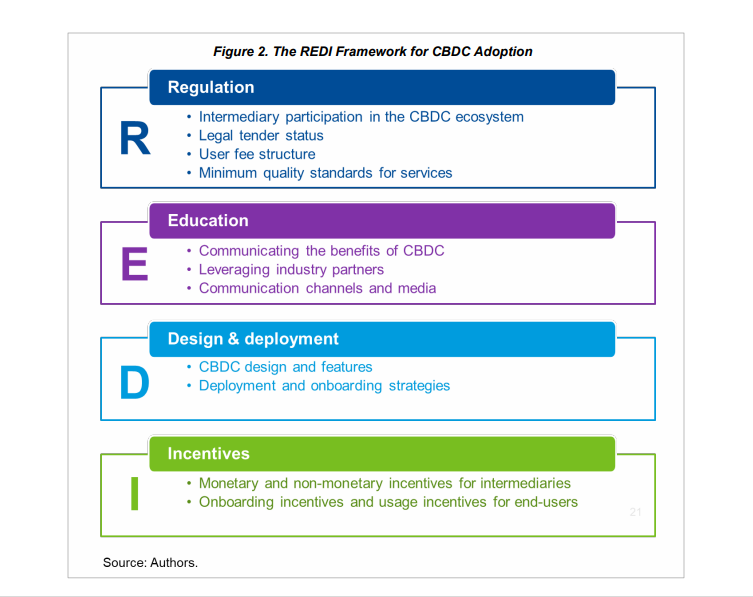

The REDI Framework

To address the various challenges identified with CDBC adoption, the IMF introduced the REDI Framework which includes regulatory strategies, education/communication initiatives, design/deployment choices, and incentive mechanisms.

REDI is further explained as follows:

- Regulation: the framework outlines potential regulatory and legislative measures that policymakers can employ to prepare for CBDC adoption. The IMF advises that central banks and relevant policymakers can set rules around intermediary participation, grant legal tender status for CBDC, govern user fees, and establish minimum quality standards for services.

- Education: the framework explains how policymakers can introduce effective communication strategies to educate stakeholders and create awareness about CBDC, to foster adoption. The IMF notes that central banks play a significant role in facilitating communication among various stakeholders, and advises that they can serve as the central point of communication, leveraging partnerships in the industry. The IMF recommends that central banks can use official portals, traditional and social media to communicate adequate information and curb misinformation about CBDC.

- Design and Deployment: the paper discusses how central banks can design CBDC and the strategies they can deploy to foster its adoption by prospective users. The IMF recommends that a CBDC design should prioritize universal access, ease of use, and security. Specifically, central banks should boost trust around privacy protection, ensure cybersecurity, and allow CBDC data to be used with user’s consent. Deployment strategies should include the implementation of selected use cases, targeting a stipulated number of users for the pilot stage, and leveraging intermediaries to create an extensive network of CBDC distribution. These intermediaries can also provide registration and KYC for users.

- Incentives: this strategy includes monetary and non-monetary incentives that central banks may consider offering to stakeholders consisting of intermediaries and end-users to encourage their active participation. The IMF recommends specific strategies as follows:

- lowering entry costs, providing subsidies, or both for consumers and intermediaries;

- minimizing fixed and variable costs for merchants and intermediaries;

- allowing for monetization of end-user data with user’ consent;

- encouraging participation of developers and Fintech firms; and

- offering onboarding incentives to users and merchants.

However, the IMF warns that monetary incentives may have fiscal consequences and the risk of them being misused.

Read also: On Nigeria’s Failing CBDC and Its Hard Lesson

The IMF has noted that the REDI framework is not universal, the same way that policies for CBDC projects are specific to countries. It advises that CBDC adoption “requires a strategic approach adapted to the unique circumstances of each jurisdiction.” This means that every country should only implement strategies that apply to its circumstances.

How countries may leverage REDI

Countries that have launched, are developing, or considering CBDCs can leverage the IMF’s REDI framework to achieve CBDC adoption. As of September 2024, 134 countries worldwide are considering CBDCs, the Atlantic Council reported. These countries should consider adapting the IMF REDI framework for implementing their projects.

Central banks of countries that are still considering to develop a CBDC should make end-user adoption their priority from the onset of their projects. Prioritizing adoption from the onset will enable countries to implement the relevant strategies, such as the IMF has recommended, to ensure that citizens adopt the CBDC. They should understand the specific needs of stakeholders.

Countries that have launched CBDC should revisit and revise their project aims, objectives, and implementation strategies to drive adoption. Nigeria, for example, should consult and collaborate with local stakeholders such as banks, payment gateways, ecommerce platforms, and the ever-growing crypto community to ensure broader adoption of the eNaira. The IMF paper discloses that 98% users have abandoned their eNaira wallets. The CBN may consider offering incentives to users and banks for eNaira transactions. For example, apart from the zero-fee transfers, they can offer 0.005% bonuses on transactions. The CBN may also partner with licensed digital assets operators to list the eNaira on their platforms.

Policymakers in countries that have launched, are developing, or are considering to build CBDC projects should consider how adoption strategies fit the policy objectives for the CBDC. Such consideration will entail central banks and policymakers defining the objectives for the project, for example, financial inclusion, resilience in domestic payments, eliminating or reducing transaction fees, among other objectives.

Lastly, central banks and policymakers should build and implement CBDC projects with specific aims and objectives. For example, the REDI Framework recommends that countries should consider the sustainability and integrity of their CBDC system, and financial stability. Specific aims and objectives will determine the potential of a CBDC project and serve as the criteria for evaluating its success.

The Metrics IMF adopted

The IMF adopted various metrics in measuring CBDC adoption across different jurisdictions. Specific metrics were applied to three categories: consumers, merchants, and intermediaries in the studied jurisdictions. The metrics for consumers included the number of individuals that registered for CBDC wallets, the volume of CBDC transactions, the value of transactions, and the percentage of first-time bank customers using CBDC. The metrics for merchants, on the other hand, included the number of merchants accepting CBDC or the transactions they processed daily. Lastly, for intermediaries, it was measured by the number of financial institutions that make CBDC available to their customers, the amount they provided to end-users, among other metrics.

About the Author: Jude Ayua is a policy analyst at CAB. A lawyer, Jude is an associate at Infusion Lawyers where he is a member of the Blockchain & Virtual Assets Group. He is also a member of the Policy & Regulations Committee of the Stakeholders in Blockchain Technology Association of Nigeria (SiBAN). Jude reports and writes on crypto policy and regulations. jude@infusionlawyers.com

Discover more from Crypto Asset Buyer

Subscribe to get the latest posts sent to your email.